The Purpose of This History Page

In the years since COVID, markets have gone through:

- liquidity explosions,

- inflation spikes,

- rate-hiking cycles,

- geopolitical shocks,

- AI-driven valuation expansions,

- and policy-induced mini-crashes (like April 2025).

Understanding these episodes in sequence helps anchor where we are now — and what risks or opportunities may rhyme with the past.

I am writing this post for new investors or anyone else who wants to know where do we stand now ? but to know the present recent past history refresh is a must. I think post covid, the market scene has changed for always as it brought huge number of new retail investors in markets through popular zero fee brokers such as robinhood.

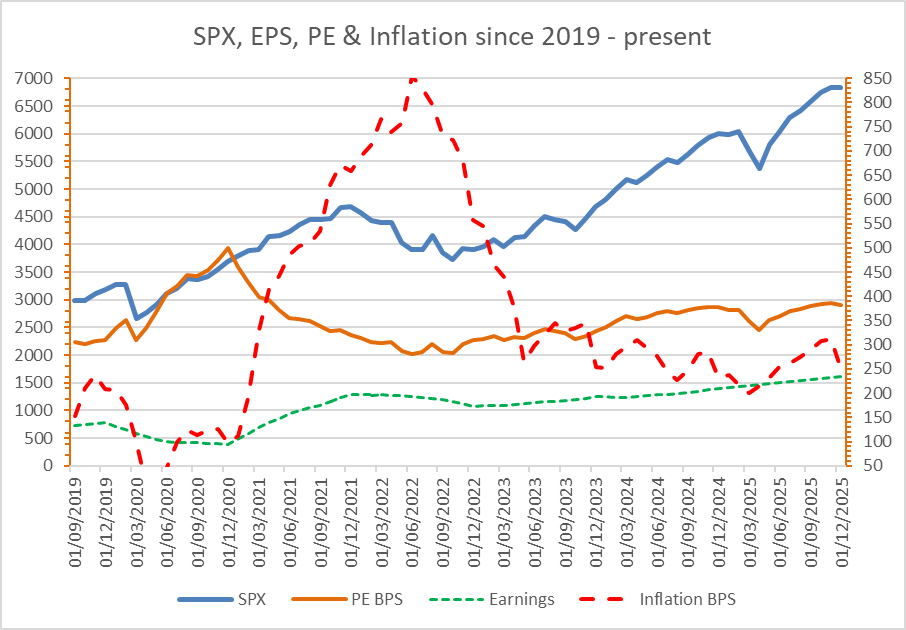

sp500 vs SP500 Eps vs inflation

sp500 vs Eps vs inflation

| Year | SPX Lvl | SP500 EPS | Inflation | PE TTM | Return %age | 10Yr Yield | Unemployment rate | Europe perf | China perf |

| 2019 | 3231 | 139 | 2,09% | 23 | 28,88 | 1.92% | 3,5% | 23,2% | 36% |

| 2020 | 3756 | 94 | 0,97% | 40 | 16,26 | 0.93% | 6,7% | -4% | 27% |

| 2021 | 4766 | 198 | 6,58% | 24 | 26,89 | 1.51% | 3,9% | 22,3% | -5,2% |

| 2022 | 3839 | 173 | 5,57% | 22 | -19,44 | 3.88% | 3,5% | -12,9% | -21,6% |

| 2023 | 4770 | 192 | 2,53% | 25 | 24,23 | 3.88% | 3,7% | 12,7% | -11,4% |

| 2024 | 5882 | 210 | 2,33% | 28 | 23,31 | 4.25% | 4% | 9% | 17,4% |

| 2025 | 6813 | 234 | 2,50% | 29 | 15,83 | 4.09% | 4% | 16,9% | 16,8% |

2020: Covid & The V-Shaped Recovery📈

The year began with the S&P 500(SPX) peaking near 3400 in February before the devastating COVID-19 flash crash. The market fell swiftly to mid-March lows near 2200, marking an end to the decade-long bull run.

- The Stimulus Response: Central banks and governments reacted with unprecedented force. The Federal Reserve cut short term rates to zero and flooded the interbanking market with reserves (Quantitative Easing-4). Simultaneously, the U.S. government provided massive fiscal stimulus (handouts and direct transfers), effectively printing new money into the real economy.

- The Great Acceleration: As lockdowns forced people home, digital adoption surged. “COVID winners” were established, including big-cap tech ($AAPL, $MSFT, $AMZN, $GOOGL, $META, $NFLX and mid-cap SaaS ($ZM, $NET, $CRWD, $SHOP. Online delivery and consumer spending $LVMH also thrived.

- The Retail Wave: The advent of zero-fee brokerages like Robinhood empowered a new generation of retail traders. Flush with time and stimulus cash, this crowd became a force, leading to a relentless market run from the mid-March lows.

- A Political Shift: Though the election loss for Donald Trump came in Q4, the market was already looking ahead to Q1 2021, anticipating an ultra-dovish fiscal policy under the incoming Biden administration, with Janet Yellen as Treasury Secretary. The SP500 surged from the 2220 lows to end the year strongly to alsmost 3700.

2021: The Mania, Inflation, and The Peak 🚀

The market run continued hard, driving the $SPX to a peak near 4800 by year-end, even as structural problems began to emerge by the end of the Yr.

- Fiscal and Monetary Fuel: The Biden administration continued the fiscal easing with direct transfers and money printing. Developed market interest rates hovered around zero or negative territory. This excess liquidity flowed everywhere: into real assets like housing and into luxury goods (Gucci bags), signaling frothiness.

- Meme Stock Mania: Market speculation reached a fever pitch. The meme stock mania gripped the market, highlighted by the GameStop short squeeze which blew up several famed hedge funds. Retail traders spent their time on forums like r/wallstreetbets Redditt board to hunt for the next gamma squeeze candidate. High-growth SaaS companies, like $NET (Cloudflare), peaked at extreme valuations (100x Sales). Cathie Wood gained notoriety on investing on speculative names in her ARK fund in name of innovation and her ARKK ETF became the new benchmark for disruptive growth. $Crypto and $Tesla also ran hard, becoming speculative darlings.

- Inflation Emerges: The fed remained dovish, with Chair Powell et al. labeling the rising prices as “transitory” and refusing to tighten monetary policy. However, by Q3 2021, inflation started to creep up due to the persistent money printing and supply chain disruptions.

- Weakening Breadth and The Last Hurrah: The “smart money” began quietly rotating out of the crowded, high-valuation names. Despite this weakening market breadth (fewer stocks participating in the rally), the large-cap tech names and a Santa Claus rally pushed the $SPX to its ultimate high of 4800.

- The Consumer Price Index finished the year at 6.71%, up from less than 1% a year prior—a clear sign that inflation was not, in fact, transitory.

2022: The Taste of Rationality and the Bear Market 📉

2022 was the year that the Fed reversed course and the long-duration growth assets of the prior cycle suffered a severe decline.

- The Inflation Truth: With COVID lockdowns largely over, the excess fiscal liquidity in the system continued to inflate retail prices. Inflation was an undeniable truth. The SPX started the year struggling, with market breadth weak, though big-cap tech initially held up.

- The Hawkish Pivot: The release of the FED minutes in January 2022 signaled a profound shift: the FED was finally taking inflation seriously and planning an aggressive sequence of rate hikes and balance sheet reduction (Quantitative Tightening). This triggered a sell-off in growth and speculative assets.

- Rate Liftoff and The Fastest Tightening Cycle: The FED began its tightening cycle in March 2022 with its first rate hike since 2018. Over the course of the year, the it unleashed the fastest rate hiking cycle in decades, including multiple unprecedented 75 bps hikes, lifting the federal funds rate from 0-0.25% to 4.25-4.5% by year-end.

- The Growth Massacre: The high-flying, long-duration assets of the zero-rate era collapsed. SaaS stocks, Midcap Software & techCrypto, and meme stocks were brutally re-rated as higher interest rates drastically reduced the present value of future earnings. The NASDAQ officially entered a bear market.

- Market Bottom and Bear Rally: The SPX dropped significantly but found an initial bottom mid-year, fueled by hopes that the FED would pivot soon (the “Fed pivot fantasy”). By October, the SPX hit its ultimate bear market low near 3491, shedding nearly 27% from its January peak. The year ended with the market pricing in the reality of sustained, aggressive monetary tightening.

2023: The Magnificent Seven and AI Mania 🤖

2023 was defined by falling inflation, a late-year Fed pivot, and a historic AI boom driven by GPT-4 and Nvidia’s explosive earnings.

Q1:

- Markets started risk-on as inflation cooled and China reopened.

- February reversed optimism as strong data pushed “higher for longer” rate expectations.

- March brought the regional bank crisis with SVB & Signature bank collapse resulting in mini banking crisis, even chatter of stress at behemoth Bank of America related to HTM bond portfolio MTM losses eroding balance sheet.

- The brief banking crisis lead to a sharp response from FED in form of stealth QE called BTFP pgm to limit the contagion. The long yields sharp rates collapsed to 4.07 to 3.3 percent on 6th april 2023.

- AI trade birth happened with release of OpenAI Chatgpt on march 14th.

Q2:

- Banking stress faded and inflation trended down.

- The entire market re-rated after Nvidia’s blowout May earnings, which ignited the global AI capex cycle and lifted semis, cloud, and megacap tech.

- By June, the Fed paused and equities surged, driven almost entirely by the “Magnificent 7.”

Q3: Rates spike & market dumps

- July optimism peaked on “soft landing” hopes.

- August–September saw a sharp bond selloff, soaring long yields, and a broad equity pullback. Yields peaked at 5% in oct2023.

- china

- China growth worries and expensive megacap valuations weighed on sentiment.

Q4: markets bottom in nov and santa Rally

- October marked the year’s lows as real yields hit cycle highs.

- Israel–Hamas war started after oct 7 attacks on Israeli civilians.

- November flipped everything: inflation surprised softer, the Fed signaled no more hikes, and markets priced early-2024 cuts.

- Huge rally in both stocks and bonds; megacap tech and AI leaders ripped back.

- December ended on euphoria with the Fed projecting multiple cuts in 2024.

Full-Year Takeaway:

2023 became the year of the soft landing and the AI super-cycle. The S&P 500 returned strongly, the Nasdaq soared, and leadership was extremely narrow—dominated by AI-linked megacaps as enterprises and cloud providers accelerated GPU spending. Macro stabilized into year-end, but micro (AI) defined the narrative.S&P ends +24%, Nasdaq +43%.

“Magnificent 7” responsible for majority of index gains.

Breadth still narrow but improving in December.

2024: Goldilocks market.

Q1 2024: The “Immaculate Disinflation” & AI Extension

The year kicked off with a continuation of the late-2023 momentum. Investors became convinced that the Fed had achieved the “soft landing”—taming inflation without causing a recession.

- January: The S&P 500 officially broke its 2022 record high, entering a confirmed bull market.

- February 21 (Nvidia’s “Drop the Mic” Moment): Nvidia again reported earnings that crushed lofty expectations. The stock surged, dragging the entire semiconductor and AI sector higher, confirming that the AI boom was not just hype but backed by massive capex spending.

- March: The Fed held rates steady but signaled that the “next move is likely a cut.” Bitcoin reached a new all-time high $73,000 ahead of its “halving” event and following the approval of Spot BTC ETFs, signaling risk appetite was broadening beyond just tech stocks.

Q2 2024: The Inflation Scare & The “Narrowing”

The smooth ride hit a speed bump as inflation data stalled, causing markets to briefly fear that the Fed might not be able to cut rates at all in 2024.

- April: US CPI data came in “sticky” (higher than expected) for the third month in a row. Bond yields spiked back toward 4.7%, triggering a swift 5% pullback in the S&P 500. The narrative shifted from “when will they cut?” to “will they hike again?”

- May/June: The panic subsided as data softened again. However, the rally became dangerously narrow. While Nvidia briefly became the most valuable company in the world, sectors like consumer staples and small caps struggled under the weight of high interest rates.

- The Divergence: We saw a major split in the “Magnificent Seven.” Tesla plummeted due to slowing EV demand and competition from China, while Apple initially lagged before announcing its own AI strategy (“Apple Intelligence”), which sent it soaring back to highs.

Q3 2024: The “Yen Carry Trade” Crash & The Fed Pivot

This was the most volatile quarter of the year, marked by a violent flash crash and the official turn of the monetary cycle.

- July 31 (The BoJ Surprise): The Bank of Japan (BoJ) unexpectedly raised interest rates to 0.25%. Simultaneously, US economic data came in weak (rising unemployment), sparking recession fears.

- August 5 (“Black Monday 2.0”): A massive global margin call occurred as the “Yen Carry Trade” unwound. Traders who had borrowed cheap Yen to buy US Tech stocks were forced to sell everything.

- The Japanese Nikkei dropped 12% in a single day (worst since 1987).

- The “VIX” (volatility index) exploded from 17 to 65 in hours.

- US markets opened deep in the red but—remarkably—bottomed that same morning and spent the rest of the month clawing back losses.

- September 18 (The Jumbo Cut): The Fed officially pivoted, cutting rates by a bold 50 basis points (0.50%) rather than the standard 25. Chair Powell framed it as a “recalibration” to protect the labor market. The S&P 500 immediately blasted to new all-time highs.*

Q4 2024: The “Trump Trade” & The Melt-Up

The final quarter was dominated by the US Presidential Election, resulting in a decisive victory that reshuffled market winners and losers.

December: The year ended in a “melt-up.” With the election over and the Fed cutting rates, cash rushed off the sidelines. The S&P 500 crossed 6,000 for the first time, capping off back-to-back 20 years.

October: Markets traded sideways/choppy as election uncertainty peaked. Bond yields began creeping up again (“bond vigilantes”) on fears of future deficits regardless of who won.

November 6 (The Election Result): Donald Trump won a decisive victory (and the popular vote), sparking an immediate “Risk-On” explosion.

Small Caps (Russell 2000) surged, betting on “America First” protectionism and lower domestic taxes.

Financials rallied on hopes of deregulation.

Crypto went parabolic, with Bitcoin shattering previous highs and racing toward 100,000$ on promises of a strategic national crypto reserve.

2025 : AI T for Tariffs – T for Trump – T for tantrums

Q1 2025 (Jan–Mar)

- Mega-cap tech / AI correction: After years of AI-driven gains, markets repriced lofty expectations following the DeepSeek launch and renewed fears of AI commoditization → Nasdaq-100 -8%, S&P -4%.

- Rotation to Europe & value: Strong Eurozone PMIs and improving earnings drove MSCI Europe +10%, as investors rotated out of expensive U.S. growth stocks.

- Treasury rally: Cooling U.S. macro data + early rate-cut bets led to falling yields → Treasuries posted positive returns.

- Post-SVB-era banking anxiety flickered: Financials underperformed as deposit-flight concerns and capital scrutiny resurfaced.

Q2 2025 (Apr–Jun)

- April “Tariff Shock” crash: Large U.S. tariffs announced across broad import categories triggered a global selloff, the sharpest since 2020 → risk assets dumped, safe havens surged.

- Supply-chain cost fears: Companies warned of margin pressure, sparking widespread de-risking in cyclicals and tech.

- Rebound by mid-May: Tariff details clarified + softer inflation data + falling yields fueled rapid recovery in equities and credit.

- Commodity divergence: Gold and havens stayed strong, but industrial metals stayed weak on global growth fears.

Q3 2025 (Jul–Sep)

- U.S. fiscal boost: “One Big Beautiful Bill” raised deduction caps → consumer-oriented sectors and domestic cyclicals gained momentum.

- Trade tensions return: U.S. reinstated tariffs on Europe, and new bilateral trade frameworks raised volatility in autos, industrials, and luxury exports.

- First Fed rate cut of cycle (-25 bps): Triggered by softening labour metrics → improved sentiment in housing, credit, and high-duration tech.

- Tech stabilizes: Post-Q1 correction, AI megacaps found footing as enterprise GPU orders remained strong despite policy noise.

Q4 2025 (Oct–Dec, so far)

- Markets stabilize: Bond selloff paused; equities saw relief as macro data steadied.

- AI bubble fears resurface: Concentration of gains in a handful of AI names + stretched valuations renewed bubble comparisons heading into 2026.

- Debt overhang becomes theme: Analysts highlighted rising global debt-to-GDP, pushing investors toward balance-sheet-strong companies.

- Cross-asset caution: Investors adopted more defensive positioning (quality, cashflow, staples) ahead of policy risk and 2026 rate-path uncertainty.

🧭 2025 Key Themes (One-Liners)

- AI goes from euphoria → normalization → selective recovery.

- Policy risk is back: Tariffs, trade blocs, and regulatory swings dominate price action.

- Rates moving down, but slowly: Yield declines support risk assets, but recession risk caps upside.

- Concentration risk grows: Equity leadership narrower than 2023–24.

- Global divergence: Europe outperforms early; U.S. rebounds late; China stays weak.